Holding Company Structure: A Practical Guide

Holding Company Structure: How to Set One Up and See It Clearly

A holding company structure is an arrangement where one parent company owns the equity of other companies and assets rather than trading itself. The parent (the “holding company”) sits at the top; the businesses, real estate, and investments it owns sit underneath as subsidiaries. The point is to separate ownership from operations, so risk, tax, and control can be organised deliberately instead of by accident. The idea is used worldwide, though the entity types and rules differ by country.

Key takeaways

- A holding company owns assets and other companies; it usually does not sell products or services itself.

- The building blocks vary by country: a limited-liability entity (a US LLC, a UK Ltd, and equivalents elsewhere) or a corporation, and many owners use several entities under one parent.

- The main benefits people seek are liability separation, cleaner ownership, and flexibility to restructure; the main costs are added admin, filings, and complexity.

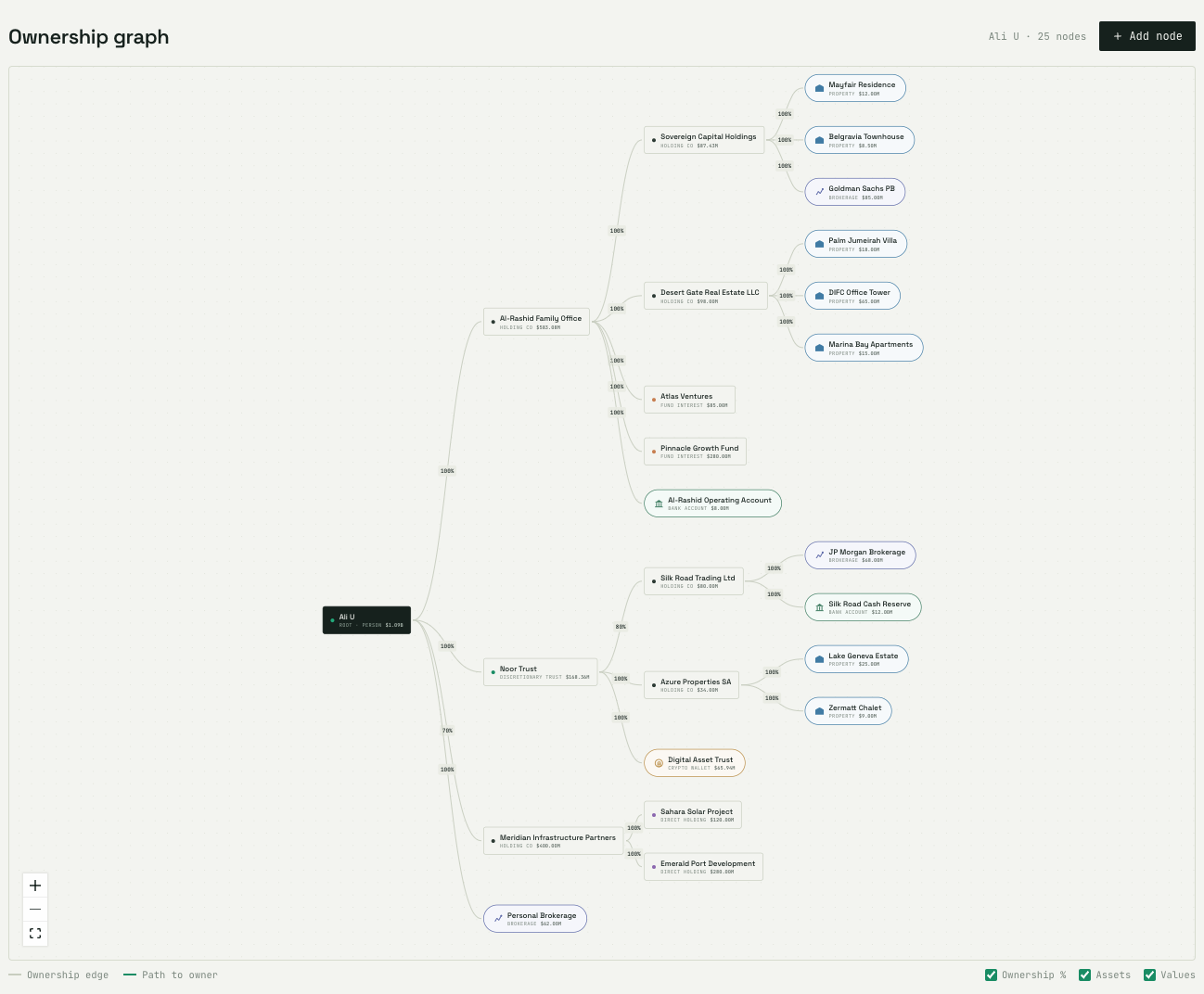

- Structure only helps if you can see it. As layers, subsidiaries, and co-owners pile up, a single ownership graph beats a folder of formation docs and a spreadsheet.

This guide covers what a holding company is, the common structures, the tax and liability basics, and how to keep the whole thing legible as it grows. It is general information, not legal or tax advice; entity types and rules vary widely by country, so confirm specifics with a qualified adviser in your jurisdiction before acting.

What is a holding company?

A holding company is a business entity whose main purpose is to own things: shares in other companies, real estate, intellectual property, or investment accounts. The companies it owns are called subsidiaries. A holding company that owns a subsidiary outright holds 100% of it; where it owns part, it holds a percentage, and the rest belongs to co-owners.

The contrast is with an operating company, which actually does the work: makes the product, signs the customers, employs the staff. In a holding structure, operations live in the subsidiaries and ownership lives in the parent. That division is the whole idea. It lets an owner ring-fence a risky trading business away from valuable assets, bring investors into one subsidiary without handing them a stake in everything, and move or sell one piece without disturbing the rest.

How should I structure my holding company?

There is no single correct shape; the right structure follows what you own and what you are trying to separate. A common pattern is a parent holding entity that owns several subsidiaries, each ring-fencing a distinct asset or line of business: one for the operating business, one for the real estate it uses, one for investments. Each subsidiary is its own legal entity, so a liability in one does not automatically reach the others.

Three questions usually decide the shape. First, what needs to be separated from what, for liability or for sale. Second, who the co-owners are, and whether they should own a single subsidiary or a slice of the parent. Third, which jurisdictions are involved, since the country (or, in federal systems, the state or province) of formation affects filing and tax. Owners of rental property, for example, often place each property in its own limited-liability entity under a parent holding company. Forming the parent and its subsidiaries then follows the ordinary company-registration steps in each jurisdiction involved.

The main types of holding company structures

Most holding structures are built from a small set of parts.

The single parent with subsidiaries is the classic: one holding entity owns several operating or asset-holding companies beneath it. The limited-liability holding company uses limited-liability entities for both the parent and the subsidiaries (a US LLC, a UK or Irish Ltd, a German GmbH, and equivalents), which many private owners prefer for the liability shield and, in some countries, lighter formality or pass-through tax. The corporate holding company (for example a US C corporation or a public limited company elsewhere) is common where outside investment, many shareholders, or share classes are involved. Some jurisdictions also offer specialised vehicles (such as the US “series LLC”) that ring-fence assets within a single entity, though availability and legal treatment vary. The names change from country to country; the pattern of a parent owning subsidiaries does not.

Trusts add another layer. A trust can sit above or alongside a holding company to hold ownership for a family, which is why owners often weigh a trust against a limited-liability entity for holding assets. The worked example below shows how these shapes fit together.

Should a holding company be a limited-liability entity or a corporation?

It depends on ownership and tax goals rather than a universal rule, and the exact entity names depend on your country. Broadly, a limited-liability entity (a US LLC, a UK Ltd, and equivalents) tends to be flexible and, in some countries, passes profits through to owners, which suits a small number of private owners. A corporation is typically taxed as a separate entity and can retain earnings and issue different classes of stock, which suits companies raising outside capital or planning many shareholders. Many structures mix the two: a corporate parent over limited-liability subsidiaries, or the reverse. (In the US this is often framed as “LLC vs C corp”; elsewhere the equivalent choice has different labels.)

The choice interacts with the “holding company vs LLC” confusion worth clearing up: an LLC (or its local equivalent) is a type of entity, while a holding company is a role an entity plays. Either kind of entity can be a holding company. The full comparison lives in holding company vs LLC. For the rules that apply to you, check your national tax authority and company registry, since both entity types and their treatment differ by country.

What are the advantages of a holding company?

The benefits cluster around separation and control.

Liability separation is the headline. Because each subsidiary is a distinct legal entity, a lawsuit or debt in one is generally contained there and does not automatically reach the parent or the sibling companies, provided the entities are run as genuinely separate. Cleaner ownership is the second: investors, partners, or family members can own a specific subsidiary rather than a stake in everything, which keeps cap tables simple. Flexibility to restructure is the third: with assets in separate entities, you can sell, gift, or refinance one piece without unpicking the whole. There can also be tax planning room depending on structure and country, though this is exactly where general guidance ends and a qualified tax adviser begins.

What are the disadvantages of a holding company?

The costs are real and mostly about complexity. Every entity you add is another formation filing, another annual report, another registered agent, another set of books, and potentially another tax return. Run the entities sloppily (mixing funds, skipping formalities) and a court can disregard the separation you paid for. And the structure gets hard to hold in your head: after a few layers, co-owners, and states, most owners genuinely lose track of who owns what and what it is all worth.

That last cost is the one people underestimate. The liability and tax benefits only survive if the structure is maintained and understood, and a structure you cannot see is a structure you cannot maintain well.

Holding companies and taxes: the basics

Tax is one of the main reasons people build a holding structure, and also the area where general information runs out fastest and where the answer depends most on your country. At a high level, the entity type drives the tax treatment. A limited-liability entity is, in some countries, a “pass-through”: profits and losses flow to the owners and are taxed on their personal returns, with no separate tax at the entity level. A corporation is more often taxed as its own taxpayer, which can mean tax at the company level and again when profits are distributed, but also allows earnings to be retained inside the company. Many tax systems give some relief to dividends moving from a subsidiary up to a parent company (participation exemptions, group relief, and similar), which is part of why corporate holding structures exist at all. The specifics, and even whether “pass-through” exists, vary widely between countries.

Sub-national tax can add a second layer in federal systems: in the US, state franchise taxes, filing fees, and income apportionment differ from state to state; other countries have their own provincial or cantonal wrinkles. None of this is a recommendation for your situation; it is the shape of the questions to take to a tax adviser who knows your jurisdictions. Start with your national tax authority (for example the US IRS, the UK’s HMRC, or your local equivalent) for the rules that actually apply to you.

Common mistakes to avoid

A few errors show up again and again. The first is treating the entities as one wallet: moving money between the parent and subsidiaries without documentation, paying personal expenses from a company account, or skipping the basic formalities. Do this and a court can “pierce the veil” and collapse the separation you built, which defeats the liability purpose. The second is over-structuring too early: standing up five entities for a single small business adds filings and cost without a matching benefit. The third is losing track of ownership: as subsidiaries, co-owners, and jurisdictions accumulate, owners quietly lose a clear picture of who owns what percentage of which asset, and what any of it is worth. That last mistake is quiet because nothing breaks, until a financing, a sale, or a dispute suddenly needs an answer nobody has. Keeping an accurate, current map of the structure is the cheapest insurance against all three.

How does a holding company make money?

A holding company earns through what it owns rather than through trading. Typical income sources are dividends or distributions passed up from profitable subsidiaries, rent from property it owns, interest and gains on investments it holds, and licensing fees where it owns intellectual property that operating companies use. It can also realise value by selling a subsidiary. Because the parent’s “revenue” is really the performance of everything beneath it, its true financial picture is a look-through of the whole tree, not a single number on one entity’s books.

Can one person own a holding company?

Yes. A single individual can own a holding company outright, commonly as a single-member LLC that in turn owns other single-member LLCs. Solo ownership keeps control simple, but it does not remove the need for genuine separation between entities: the same discipline about separate accounts, records, and formalities applies whether there is one owner or ten. As soon as a co-owner, a trust, or a second class of interest enters, the ownership math stops being obvious and the case for mapping it grows.

Holding companies, trusts, and jurisdictions

Real structures rarely stay tidy. A parent entity in one country may own subsidiaries formed in others; a family trust may sit above the parent; a fund interest or a foreign entity may hang off a branch. Each addition is defensible on its own, and each one makes the total picture harder to see. Multiple jurisdictions also mean multiple rulebooks, so a liability or tax statement that is true in one country may not hold in another. This is why naming the jurisdiction matters whenever you reason about a specific rule, and why “ask my lawyer” so often becomes the only way anyone knows the current shape.

How to keep your structure legible as it grows

A holding company structure is only as useful as your ability to see it. The failure mode is not the diagram you drew on day one; it is month eighteen, when formation docs are in a drawer, the cap table is in an email, valuations are in a spreadsheet, and the rest is in your accountant’s head.

Mapping the structure fixes that. Pulling every company, subsidiary, trust, and asset into one ownership graph shows how it all fits together, values each holding through every layer (so you see effective ownership, not just headline percentages), and lets you model a change before you commit to it. That is what HoldCo is built to do: it maps your entities, values everything look-through, and keeps your true net worth current, so the structure you designed is the structure you can actually see. It also lets you move an asset or add a co-owner and watch every number downstream update before you commit, which turns restructuring from guesswork into something you can check first.

Frequently asked questions

Is a holding company the same as a parent company? In practice the terms overlap. “Parent company” describes any company that owns another; “holding company” usually implies the parent exists mainly to own rather than to trade.

Do I need a holding company? Not necessarily. It earns its keep when you have multiple assets or businesses to separate, co-owners to keep straight, or a plan to restructure. For a single simple business, it can be overhead you do not need yet.

How many subsidiaries can a holding company have? There is no fixed limit; the practical ceiling is how much administration and oversight you can sustain, which is another reason to keep the structure mapped.

Which country or state should I form a holding company in? It depends on where you operate and hold assets. Some owners form in their home country for simplicity; others use jurisdictions known for their entity law or fees. The trade-off is that operating somewhere usually means registering there anyway, so a second jurisdiction of formation can add filings rather than remove them, and can raise cross-border tax questions. It is a question for a qualified legal and tax adviser, weighing your specific assets and where they sit.

Does a holding company protect my personal assets? Entities can separate business liabilities from each other and from you, but that protection depends entirely on running them properly: separate accounts, real records, and no mixing of funds. Structure alone does not create protection; discipline does. Asset protection also has legal limits and differs by country, so treat any specific plan as one to confirm with a qualified lawyer in your jurisdiction.

What is the difference between a holding company and a subsidiary? They are two ends of the same relationship. The holding company is the parent that owns; the subsidiary is the company that is owned. One entity can be both at once, a subsidiary of the company above it and a parent to the companies below it, which is exactly how multi-layer structures form and why look-through valuation matters.

This article is for general information only and is not legal, tax, or financial advice. Structures, entity types, and rules vary widely by country and situation; consult a qualified legal, tax, or financial adviser in your jurisdiction before acting.

Ready to see your structure in one place? Request early access to HoldCo.